How the Asian Financial Crisis and Global Financial Crisis Shaped Singapore’s Property Market (Updated)

- Stuart Chng

- Dec 24, 2025

- 6 min read

One of the most common questions I receive from readers is whether I’ve studied how past economic crises—specifically the Asian Financial Crisis (AFC) and the Global Financial Crisis (GFC)—affected Singapore’s property market, and how those periods compare to what we are experiencing today.

The short answer is: yes.

In fact, I shared my research internally with my team earlier this year, before the Circuit Breaker began. While it’s impossible to draw perfect comparisons between crises—each unfolds under very different conditions—studying historical market behaviour can still offer perspective and, for many, a sense of grounding during uncertain times.

As humans, we naturally seek reference points during distress. Understanding how markets recovered in the past doesn’t guarantee outcomes today, but it helps us make more rational decisions instead of emotional ones.

In this article, I’ll walk you through how Singapore’s residential property market responded during the AFC and GFC, and what insights we can cautiously take forward.

The Asian Financial Crisis (1997–1999)

Impact on Private Residential Property Volumes

The AFC hit Singapore in July 1997, and transaction volumes declined almost immediately.

Private property sales volumes fell sharply across all regions but began to recover around nine months later.

PRIVATE MARKET (VOLUME) DURING AFC

CCR (Core Central Region): –42%

RCR (Rest of Central Region): –59%

OCR (Outside Central Region): –64%

The relatively milder decline in the CCR likely reflected stronger holding power among wealthier buyers, while mass-market buyers adopted a wait-and-see stance amid job insecurity.

When confidence returned around March 1998, transaction volumes rebounded aggressively:

CCR: +45% month-on-month

RCR: +94%

OCR: +286%

This surge was driven largely by pent-up demand in the mass market.t buyers who had greater visibility and confidence in a recovery by March 1998.

Price Movements During the AFC

By the trough:

Landed properties: –38%

Non-landed private homes: –35%

PRIVATE NON-LANDED AVERAGE PSF CORRECTION BY REGION

Regionally, non-landed price corrections were:

OCR: –30%

RCR: –45%

CCR: –42%

The AFC affected all segments relatively evenly, from mass-market to prime areas.

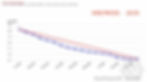

PRICES REBOUNDED TO PAST HIGHS WITHIN 14 MONTHS OF BOTTOMING OUT

When the green shoots of recovery started sprouting in Nov 1998, prices rebounded near to pre-crisis highs within 13-14 months of the bottoming out.

Land properties appreciated by 48% and non-landed condominiums and apartments appreciated by 71%.

In total, it took approximately 2 years and 4 months for the property market to reach a full recovery to previous price heights.

HDB VOLUME TREND DURING AFC

HDB Market During the AFC

Unlike the private sector, HDB transaction volumes increased during the AFC.

This was largely due to:

Private property owners downgrading

Affordability pressures pushing demand toward public housing

HDB AVERAGE PSF PRICE TREND DURING AFC

Despite stronger volumes, sentiment remained weak and HDB prices still corrected by about 22.5%.

What stood out, however, was the recovery timeline.

👉 HDB prices took approximately 11 years to return to pre-AFC levels.

PRICE RECOVERY OF HDB MARKET TOOK 11 YEARS AFTER AFC

This prolonged stagnation became known as a “lost decade” for many HDB owners and partly explains why subsequent investment cycles saw stronger preference for private property ownership.

The Global Financial Crisis (2008–2011)

Transaction Volumes During the GFC

The GFC had a more severe and prolonged impact on transaction volumes.

PRIVATE PROPERTY MARKET SALES VOLUME DURING GFC

Private property sales fell dramatically and only showed meaningful recovery around 19 months later, in March 2009.

Declines by region:

OCR: –78%

RCR: –86%

CCR: –89%

Once confidence returned, volumes rebounded strongly month-on-month:

OCR: +124%

RCR: +183%

CCR: +191%

Despite this rebound, volumes remained below pre-crisis highs for some time.

PRIVATE PROPERTY MARKET (AVERAGE PSF PRICE) DURING GFC

Price Behaviour During the GFC

This time, landed properties demonstrated far stronger holding power.

Landed homes: –18%

Non-landed private homes: –42%

Prices bottomed out after 18–19 months, longer than during the AFC.

RECOVERY IN PRIVATE NON-LANDED MARKET TOOK 14 MONTHS AFTER BOTTOMING

Notably:

Landed prices recovered to pre-crisis levels within 4 months of bottoming out

Non-landed prices took 14 months, similar to the AFC

Overall, full recovery took approximately 2 years and 8 months.

PRIVATE NON-LANDED AVERAGE PSF CORRECTION BY REGION

Regional Differences in the GFC

Unlike the AFC, the GFC disproportionately affected the higher-net-worth segments.

Non-landed price corrections by region:

CCR: –46%

RCR: –33%

OCR: –17%

This reflected heavier exposure to financial markets among prime-area buyers.

HDB TRANSACTION VOLUME TREND DURING GFC

HDB PRICE TREND BY AVERAGE PSF DURING GFC

HDB Market During the GFC

HDB transaction volumes were largely resilient.

There was a brief dip over two months—consistent with typical year-end slowdowns—but volumes recovered quickly.

More notably, HDB prices rose by about 20% by March 2009, even as private prices were still correcting.

This created strong upgrading opportunities, which subsequently fuelled the 2009–2013 property bull run.

What This Means Moving Forward

Looking back, April 7, 2020—the start of the Circuit Breaker—will likely mark the beginning of this market cycle’s defining chapter.

That said, today’s crisis is fundamentally different:

Massive global liquidity injections

Extensive fiscal support (including Singapore’s resilience budgets)

Record-low interest rates

These factors have helped stabilise employment and asset prices—at least for now.

In recent months, transaction volumes across most segments have softened, with selective discounts emerging in both new launches and the resale market.

While some projects have seen healthy take-up amid incentives, broader activity remains subdued.

My personal view is that resale properties, particularly larger and older units with higher quantum, may face greater downside pressure compared to new launches supported by developers with strong balance sheets.

Developers are incentivised to avoid sharp price corrections that could destabilise the wider economy. Resale owners, however, may find themselves more exposed once temporary relief measures expire.

Should You Wait or Act?

This is not a call for inaction.

History shows that crises often present the best opportunities—but only for those who are prepared.

Property remains one of the few asset classes that:

Allows safe leverage

Is less prone to margin calls

Cannot go to zero

Compared to equities, which can react violently to disruption or mismanagement, property offers stability, time, and optionality—especially for those balancing family, work, and long-term planning.

Personally, I am actively evaluating opportunities now, as true value tends to surface most clearly during uncertain periods.

Final Thoughts

No two crises are the same. But understanding how markets behaved during the AFC and GFC gives us a valuable framework for thinking clearly, managing risk, and recognising opportunity.

If you’d like to learn how I assess market entry timing and build margins of safety, I recommend reading “When Is the Right Time to Enter the Property Market?”

I hope this analysis helps you gain clarity as you plan your next steps in your property investment journey.

Need an opinion on your property investment plans, the best buys available or help marketing your properties?

Get a 1-time free 30 min Property Wealth Planning consultation with Stuart and his team of advisers.

A PWP consultation includes:

- An in-depth financial affordability assessment and timeline planning

- Highly relevant investment insights

- A clear and customised investment road map

- A curated list of best buys in today's market with good growth potential & minimal risks

- Selecting units with the highest potential in a new launch project

- Advice on marketing and getting a buyer for your property fast

- Has your property stagnated in price? What are the reasons and options you have?

Stuart Chng, Executive Group District Director at Huttons, is a renowned leader and personality in the real estate industry.

He adores music and can play a few instruments decently without upsetting his neighbours. When not doing so, he enjoys pillow fighting with his son and coming up with silly puns which barely amuses his wife.

Professionally, he is a licensed real estate agent, investor, team leader, speaker and columnist for several property newsletters and blogs and is often quoted in media interviews on 938FM, Channel 8, PropertyReport, PropertyGuru and other publications. Throughout his career, he has helped many clients grow their wealth through selecting great property investments and managing their portfolios actively. Read his clients' reviews here.

Stuart has also coached many top million dollar producing agents from different real estate agencies in Singapore. Read his agents' reviews here.

Relevant Reading: